Key terms in this article

What is the Prompt Payment Code?

The Prompt Payment Code was a voluntary scheme for large UK businesses to commit to paying suppliers on time. It was replaced by the Fair Payment Code in December 2024, which awards gold, silver and bronze ratings based on actual payment performance.

Who is the Small Business Commissioner?

The Small Business Commissioner is a UK statutory officer who helps small firms resolve payment disputes with larger customers. The 2025-26 reforms will extend the Commissioner’s powers to issue financial penalties to repeat offenders.

What is statutory interest on late payment?

Statutory interest is the rate set by the Late Payment of Commercial Debts (Interest) Act 1998. It is 8% above the Bank of England base rate, plus a fixed compensation amount of £40 to £100 depending on the size of the debt. Suppliers can claim it on commercial debts paid late by raising a new invoice for the interest and the fixed amount; it is a right the supplier chooses to exercise, not an automatic add-on.

Update, May 2026: the Small Business Protections (Late Payments) Bill was confirmed in the King’s Speech on 13 May 2026. See our follow-up: The Late Payments Bill Confirmed: What Resellers Should Watch For. The post below was written in October 2025 against the July 2025 Government announcement and the open consultation, and remains accurate for that context. The formal consultation response was published later (last updated 24 March 2026).

What Are the 2025-26 Late Payment Reforms?

In July 2025 the UK government announced the toughest crackdown on late payments in over twenty-five years (GOV.UK, 2025). The reforms cap commercial payment terms at 60 days, give the Small Business Commissioner new powers to fine repeat offenders, and propose new board-level reporting on supplier payment practices.

Late payment costs the UK economy around £11 billion a year on official Government figures, with around £26 billion owed to small businesses at any given time. Secondary industry estimates, framed differently, put the cumulative SME exposure as high as £70.4 billion (startups.co.uk, 2025). For telecoms resellers, the reforms matter on both sides of the relationship: as a supplier chasing customers who pay late, and as a customer of your own wholesale providers whose payment terms may now also be capped.

Key Takeaways

- Late payment costs the UK economy around £11bn a year on Government figures, with around £26bn owed to small businesses at any time; secondary industry estimates put the average exposure per SME at around £12,357 (startups.co.uk, 2025)

- The government consultation closed in October 2025; legislation is expected in the 2026 King’s Speech (Tackling Poor Payment Practices consultation, GOV.UK, 2025)

- Maximum standard terms will be capped at 60 days, with the goal of 45 days within five years

- Commercial contracts will be required to include a default right to statutory interest, removing the ability for stronger parties to negotiate it away; suppliers still decide whether to charge it (proposed)

- Audit committees and boards of larger companies will face new reporting duties on supplier payment practices

- The Small Business Commissioner will be able to issue financial penalties

- Charging statutory interest works on paper; in practice, suppliers rarely use it. Automated chasing letters work far better

Why the Reform Matters Now

Late payment is structural in the UK economy. Around 50% of SMEs are paid late on a regular basis. For small telecoms resellers, the impact is concentrated: a few large business customers running 60 to 90 days late can swing the cash position of the whole reseller business.

The 2025-26 reform package does three things that change the dynamic.

It caps standard payment terms. Large customers cannot contract a small supplier onto, say, 120-day terms. 60 days becomes the legal maximum on standard contracts, with the policy intent to drop further over the next five years.

It strengthens the statutory interest right. The proposals require commercial contracts to include the statutory interest right by default, so stronger parties cannot negotiate it away. Suppliers still decide whether to claim it on any given overdue invoice. Customers who routinely pay late should expect more suppliers to actually charge it.

It puts the topic in front of the board. Larger companies’ audit committees and boards face new reporting obligations on supplier payment practices, so late payment becomes a governance-level matter, not just a finance-team one. The reputational cost of being on the wrong list goes up.

What This Means for a Telecoms Reseller as a Supplier

If you supply telecoms to small or mid-sized businesses, the reforms work in your favour. The customers who routinely paid you 75 days late will increasingly face the choice of paying you on time or seeing the interest stack up. The Small Business Commissioner will, in time, be able to fine the worst offenders directly.

If you supply telecoms to a large enterprise, the reform also works in your favour but more slowly. Large customers will adjust their payment runs over the course of 2026 and 2027. Watch the Fair Payment Code ratings; the gold-tier accreditation is a signal that the customer is paying suppliers within 30 days.

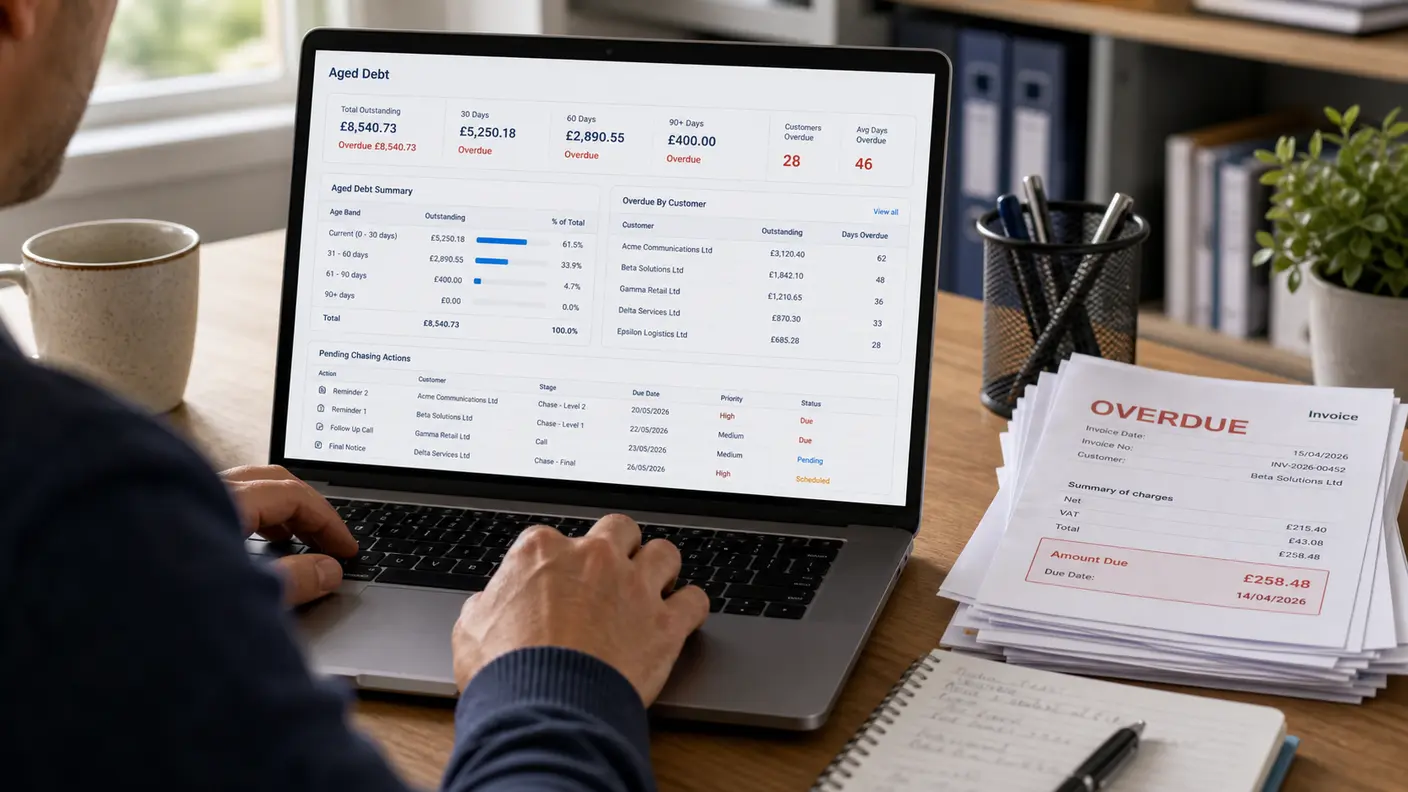

What This Means for Your Own Aged Debt

The reverse perspective. If a customer of yours is now subject to a 60-day cap and chooses to pay you on the 59th day every time, your average days-to-pay goes up, not down. Your cash collection patterns will shift through 2026 and you should plan for it.

From our experience: charging statutory interest sounds attractive but is rarely used in practice. The platform calculates it correctly, but most resellers turn it off. Customer relationships matter more than the marginal cash, and the recovery rate from chasing interest is small. What does work, reliably and repeatedly, is semi-automated chasing letters. Three letters at fixed intervals, with the wording adjusted by debt age, recovers more cash than any interest charge ever has for our customer base. The billingplatform.uk post on automated late-payment chasing covers how we have customers set this up.

What to Update on Your Side

A short list of things worth doing in the next few months.

Check your terms. If your standard terms still say 30 days, you are already aligned with the reforms. If they say longer, you may want to tighten them.

Adopt the Fair Payment Code if you can. Small businesses can register too. The gold tier requires paying suppliers within 30 days. This is a positioning signal for B2B customers who care.

Switch on automated chasing. A first reminder, a stronger second reminder and a final notice each work better than ad-hoc emails. Most billing platforms support this natively.

Review aged debt monthly. Anything older than 60 days is exposed under the new regime. Anything older than 90 days is a phone call, not a letter.

Decide your interest policy and stick to it. If you choose not to charge statutory interest, that is a relationship decision and is fine. But make it a deliberate decision, not an oversight.

Where the Real Recovery Comes From

The honest answer is that recovery rates correlate with the number of times you ask, not the rate of interest you charge. Three letters at fixed intervals, generated automatically, with a clear next step at each escalation, will move more cash than any statutory-interest line item on its own.

Resellers who treat dunning as an automated workflow, not as a series of awkward phone calls, collect faster and have better customer relationships at the same time. The late-payment automation post on billingplatform.uk walks through the specific letter sequence, the gaps between them and how the platform tracks responses.

How SAFE Billing Platform Helps

SAFE applies statutory interest automatically if you want it on, or leaves it off if you prefer to handle late payment through relationships and letters. The payment collection service covers GoCardless Direct Debit and card payment options if you want to move more customers onto automated payments. Either way, the billing run guide covers the monthly cycle including the dunning step, and aged debt reporting is built into the standard KPI screens. If you want a walk-through against your own customer base and current aged debt profile, the contact form is the quickest way in.